From FrankenStack to Customer-Centricity

Steven BakkerStrategist at New Black

Why Retailers Must Simplify Technology to Truly Engage Customers

Many retailers operate on fragmented IT landscapes — FrankenStacks — built from years of isolated decisions and patchwork tools. This Insight reveals how Unified Commerce enables faster innovation, lower operational cost, and true customer-centric execution by replacing architectural complexity with strategic coherence.

In this Insight, we reveal the hidden strategic drawbacks and operational barriers associated with FrankenStacks. Leveraging extensive industry research and practical retail case studies, we assess four prevalent technology strategies: continuing with a FrankenStack, upgrading ERP solutions, consolidating through Best-of-Breed approaches, and transitioning fully to Unified Commerce.

Our analysis provides concrete, data-driven insights into how each strategy impacts critical aspects like operational efficiency, compliance, security, productivity, and - most importantly - the retailer’s ability to truly understand and engage customers. Ultimately, this Insight reveals that simplifying technology architecture through a Unified Commerce platform is not just beneficial; it is strategically essential for any retailer seeking sustained competitive advantage, operational agility, and genuine customer-centric innovation.

“A FrankenStack isn’t just complexity - it’s systemic self-sabotage”

Executive Summary

From Patchwork to Aligned Architecture: Why Unified Commerce is Retail’s Strategic Imperative

No retailer planned on building a FrankenStack - but they all ended up with one. Years of incremental IT decisions, siloed tools, and ERP-centered architectures have created fragile, costly, and rigid technology ecosystems that can’t keep up with today’s customer demands.

This Insight Reveals the Strategic Drawbacks of maintaining a FrankenStack

- Escalating operational costs

- Slower time-to-innovation

- Disjointed and inconsistent customer experiences

The Structural Advantage of Unified Commerce

Of the available strategies, Unified Commerce stands out as the most resilient, scalable, and customer-centric.

By consolidating fragmented (Best-of-Breed) systems and decoupling customer experience from rigid back-office structures, retailers unlock a more agile and coherent foundation for growth. This shift enables:

- Real-time, channel-agnostic customer engagement

- Significant reduction in operational costs

- 5-10x faster time-to-market

We Evaluated Four Common Strategies Retailers Follow

- Maintaining the FrankenStack: Low initial investment, high long-term cost

- Upgrading to modern ERP suites: Improves stability but retains complexity

- Best-of-Breed integration: Promises flexibility, but often rebuilds a new FrankenStack

- Unified Commerce platforms: Consolidates architecture for real-time, customer-first operations

Conclusion: FrankenStacks Do Not Just Cost Money - They Cost Relevance

Retailers who fail to modernize their architecture will increasingly struggle to meet even the most basic expectations of today’s channel-agnostic customer.

“You can’t be customer-centric on an architecture that isn’t”

The Strategic Challenges Behind the FranckenStack

You might be at a crossroad. Most retailers operate on FrankenStacks - fragmented system landscapes built over years of incremental upgrades and replacements. What once worked now slows you down, drives up cost, and breaks the customer experience. This growing complexity forces a choice: keep patching or rethink the foundation. Most retailers take one of four strategic paths - each with very different outcomes.

- 1.

Continuing with the Existing FrankenStack

Maintaining existing, fragmented systems may provide short-term flexibility, low upfront investment, and specialized functionality. However, retailers typically face rising long-term operational costs, decreased innovation capability, and increasing technical debt.

- 2.

ERP Suite Upgrade (Consolidation and Standardization)

Centralizing processes within an ERP ecosystem offers operational stability, predictable costs, and improved oversight. Nonetheless, ERP inherently require additional functional & customer-facing layers - such as CRM, POS, or e-commerce - to effectively engage customers. Due to these required integrations, ERP-centric solutions inevitably maintain or recreate elements of the original FrankenStack, limiting responsiveness and strategic agility.

Retailers often begin by upgrading or expanding their existing ERP system, aiming to standardize operations and reduce complexity. However, because ERPs typically lack flexible customer-facing functionalities, this step generally leads to the next strategy: a further consolidation through Best-of-Breed solutions.

- 3.

Consolidation by Best-of-Breed Solutions (BoB)

Retailers commonly attempt to address ERP limitations by integrating specialized BoB tools and platform technologies, attracted by their innovation and fit by purpose potential. Although these modular solutions initially appear advantageous, they introduce high integration complexity, hidden operational costs, and substantial governance challenges. Consequently, retailers frequently find themselves inadvertently recreating a new form of FrankenStack, dependent once again on ERP at its core.

Research by Gartner (2024) indicates that 60% of retailers pursuing BoB consolidation experience significant governance complexity and integration overhead, effectively negating the intended operational simplicity.

- 4.

Unified Commerce Suite

Implementing a fully integrated omni-channel platform represents the most sustainable strategy to prevent or significantly reduce the FrankenStack. By centralizing data and removing unnecessary layers, this approach enhances operational efficiency, reduces complexity, and enables superior customer experiences. Within this strategy, two distinct ERP configurations are typically considered:

- ERP-Heavy Unified Commerce

ERP retains substantial internal operational control, carrying the risk of retaining legacy complexity and limited agility. - ERP-Light Unified Commerce

In this architecture, the ERP is streamlined to focus on essential back-office functions - such as General Ledger and procurement - while all operational control and customer interactions shift to the commerce platform. This separation reduces architectural complexity and enables true real-time responsiveness across all channels.

- ERP-Heavy Unified Commerce

How ERP Architectures Gave Rise to The Frankenstack

The term FrankenStack describes the complex IT landscape frequently encountered within retail organizations, consisting of multiple independent legacy technologies, customized applications, custom-built solutions, middleware and integrations. Individually, these components effectively address specific operational or functional requirements. However, collectively they create substantial operational complexity, elevated integration costs, decreased agility, and significant strategic limitations.

Typical Characteristics of a FrankenStack

- Multiple legacy systems running simultaneously.

- Complex integrations.

- Fragmented and siloed data, leading to data inconsistencies.

- High vendor management overhead and complex integration governance.

Recognized FrankenStack Challenges Across Retail

Limited organizational agility | 74% |

Escalating operational costs | 72% |

Complex integrations | 69% |

Fragmented and siloed data (data inconsistencies) | 65% |

Multiple legacy systems running simultaneously | 63% |

High vendor management overhead | 60% |

Integration governance complexity | 57% |

These are the most frequently reported issues in organizations operating on fragmented, legacy-based architectures.

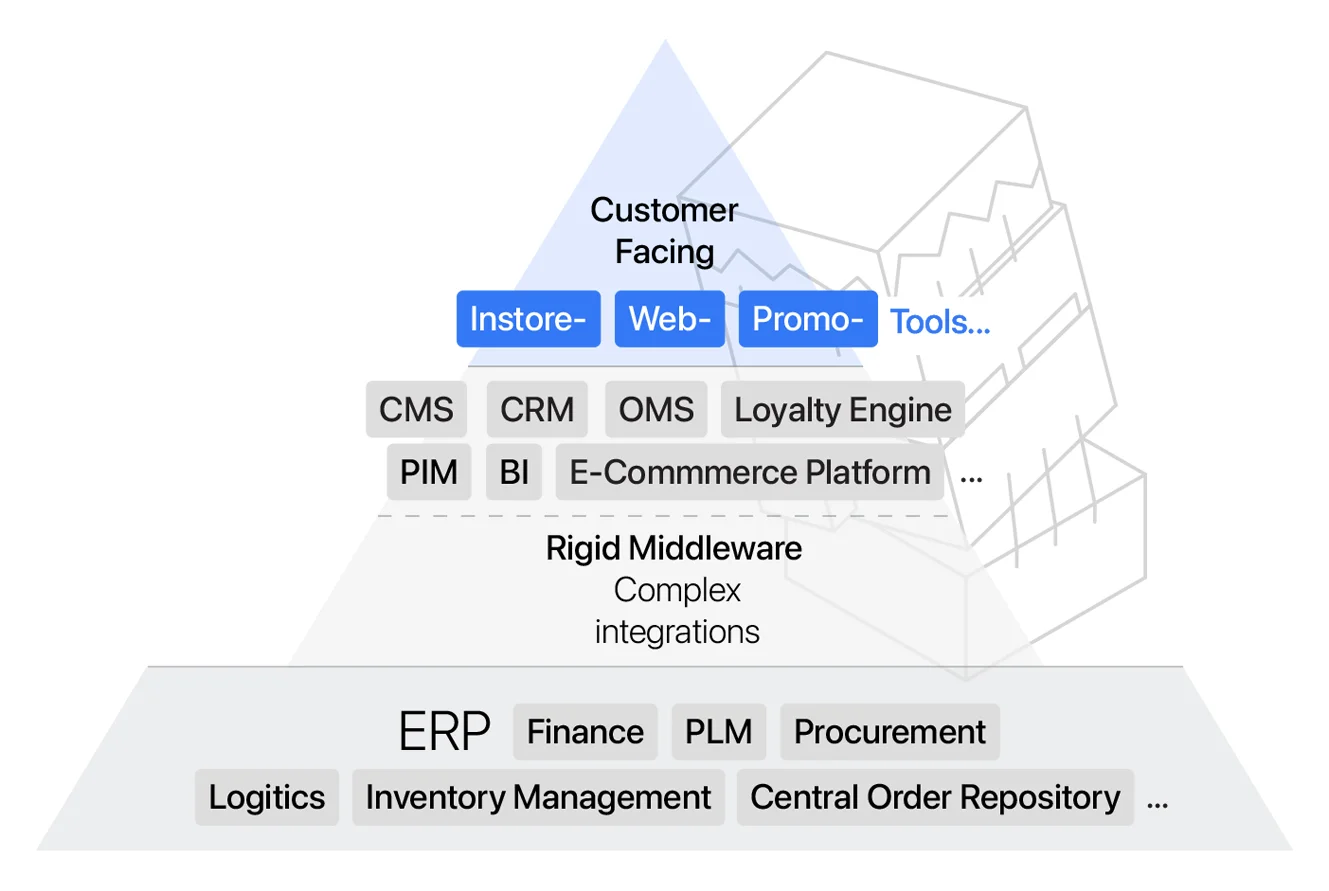

Classic IT Enterprise Architecture Model: The FrankenStack Pyramid

Historically, retailers structured their IT enterprise architecture around ERP systems. ERP, positioned as the foundational layer in this pyramid, primarily addresses internal operational control rather than customer interactions.

Consequently, multiple layers specialized, tools and applications - such as Mobile POS, Clienteling, Instore Inventory Management, Task Management, and Promotion Engines, among others - are continuously layered above the ERP system. Together, these cumulatively create the complexity known as the FrankenStack.

What ERP Was Built For - and Why That’s a Problem Now

Initially, ERP systems were widely adopted within retail because they provided stability, standardized processes, and centralized internal operational control. Retailers trust ERP systems as a comprehensive solution to manage most, if not all, critical business processes. However, ERP solutions were originally built around internal business logic and standardized processes, without the flexibility or real-time responsiveness required for customer-facing operations.

As retail evolved - driven by increasing consumer expectations, diverse customer journeys, and real-time omnichannel interactions - it became clear that ERP systems could not deliver these new capabilities directly to customers. Retailers responded by adding layers of specialized Best-of-Breed (BoB) solutions, middleware, and custom integrations on top of ERP, aiming to bridge the gap between their internal systems and the customer.

ERP systems inherently prioritize internal control, efficiency, and standardized business processes over agility and real-time customer responsiveness. The necessity to build additional layers on top of ERP to enable customer interactions inevitably leads to the formation of a FrankenStack.

- 1.

ERP’s original intent

ERP is designed for internal business process standardization and operational control, not for enabling customer engagement.

- 2.

Inherent limitations

ERP typically operates in batch-processing mode, rendering it incapable of delivering real-time, personalized insights and customer experiences.

- 3.

Additional layers

Retailers continuously introduce specialized CRM, POS, OMS, e-commerce platforms, and other customer-facing tools, inadvertently creating substantial integration complexity and operational challenges - the essence of a FrankenStack.

“Retailers on average operate over 120 applications - each”

Range of Applications Managed by Retail Organizations

Application Layer | Range of Applications |

|---|---|

Customer-Facing Systems Web engine / Consumer App / POS, mobile POS, CRM, clienteling, loyalty, e-commerce, OMS, payment gateways, digital marketing, analytics, personalization engines, etc. | 25~55 |

Operational & Employee Enablement Tools Task management, workforce management, store inventory management, pricing & promotion, markdown optimization, scheduling, compliance reporting, etc. | 18~35 |

Custom-Built Applications & Utilities Custom reporting, in-house databases, legacy data management, data warehouses, custom dashboards, etc. | 10~30 |

Middleware & Integration Layers Custom APIs, ESB, messaging queues, ETL tools, API gateways, integration monitoring, etc. | 5~12 |

ERP & Legacy Core Systems ERP finance, inventory, warehouse management, logistics, forecasting, procurement, batch processing, etc. | 8~18 |

Total Average per Retailer | 66~152 |

Illustrative data based on Gartner Retail IT Complexity Benchmark, Deloitte Retail IT Survey, IDC Retail Insights, and Forrester Retail Technology Landscape, 2024

Justifications for ERP-Centric Thinking

ERP was originally adopted in the 1980s to streamline internal processes, but its limitations became increasingly clear as retail evolved. Still, many organizations continued to justify ERP-centric architectures - even as complexity and cost increased. The table below outlines the most common justifications for holding on to outdated ERP-driven systems, despite growing strategic misalignment with modern retail needs.

Justifications | % of Retail Organizations | Description |

|---|---|---|

Short-term Investment Prioritization | 68% | Retaining legacy infrastructure often requires less immediate investment commitment compared to large-scale digital transformations, especially appealing in asset-heavy industries facing tight cash-flow constraints. |

Organizational Inertia & Change Management Complexity | 66% | Organizations sometimes struggle internally with large-scale digital transformations due to limited internal alignment, inadequate skills, conflicting internal interests, or cultural resistance. Effective change management demands a clear strategic vision, cohesive leadership, and dedicated resources—elements often lacking—perpetuating reliance on FrankenStack. |

Lack of Strategic Ambition | 62% | Some retail organizations lack the strategic vision or ambition to proactively embrace transformative changes. They may underestimate market shifts, maintaining legacy systems despite competitive disadvantages, even as peers relying on outdated approaches lose market share or exit the market. |

Operational Risk Minimization | 55% | Incremental updates present lower immediate disruption compared to comprehensive migrations, ensuring continuity of critical operations—particularly in sectors where downtime is prohibitively costly. |

Asset Write-off Avoidance (Depreciation Risk) | 51% | Early replacement of legacy systems often triggers substantial financial write-offs. Leaders may hesitate to assume responsibility for large-scale asset depreciation, preferring instead to postpone investments to align with existing depreciation schedules. |

Specialized Legacy Functionality | 45% | Legacy systems often offer highly customized capabilities tailored to unique operational needs. Industries such as aerospace, defense, or complex manufacturing may genuinely rely on deeply customized legacy solutions. |

Regulatory Compliance | 41% | In heavily regulated sectors (e.g., pharmaceuticals, defense contracting), existing systems effectively manage stringent local regulatory frameworks. Replacing or modifying these could pose substantial compliance risks. |

These justifications reflect prevalent internal perceptions and beliefs within retail organizations rather than objectively validated reasons. In practice, relying on these arguments often perpetuates outdated technology choices, contributes to competitive disadvantage, and significantly increases the risk of business failure in today’s dynamic retail environment.

Post-Bankruptcy Reflections from Retail Executives on Strategic Actions

Strategic decisions about architecture rarely seem urgent - until it’s too late. Based on over 35 years of experience, industry research, and direct conversations with global retail leaders, we’ve identified a consistent pattern of post-bankruptcy reflections. These frequently cited regrets point to delayed action, underinvestment in customer-centricity, and over-reliance on FrankenStacks as key contributors to long-term failure.

Question - What actions might have prevented long-term failure?

Should have invested earlier in customer-centric focus

74%

Should have been more ambitious about a digital transformation strategy

69%

Should have had a stronger commitment to organizational change management

67%

Should have had better financial prioritization for strategic technology investments

63%

Should have improved internal alignment and put less focus on internal politics

59%

Should have been more proactive towards cultural change innovation

55%

Should have phase-out legacy systems faster (FrankenStack)

52%

Should have had the willingness to write off legacy technology assets earlier

47%

“Strategic delay is rarely visible - until it becomes irreversible”

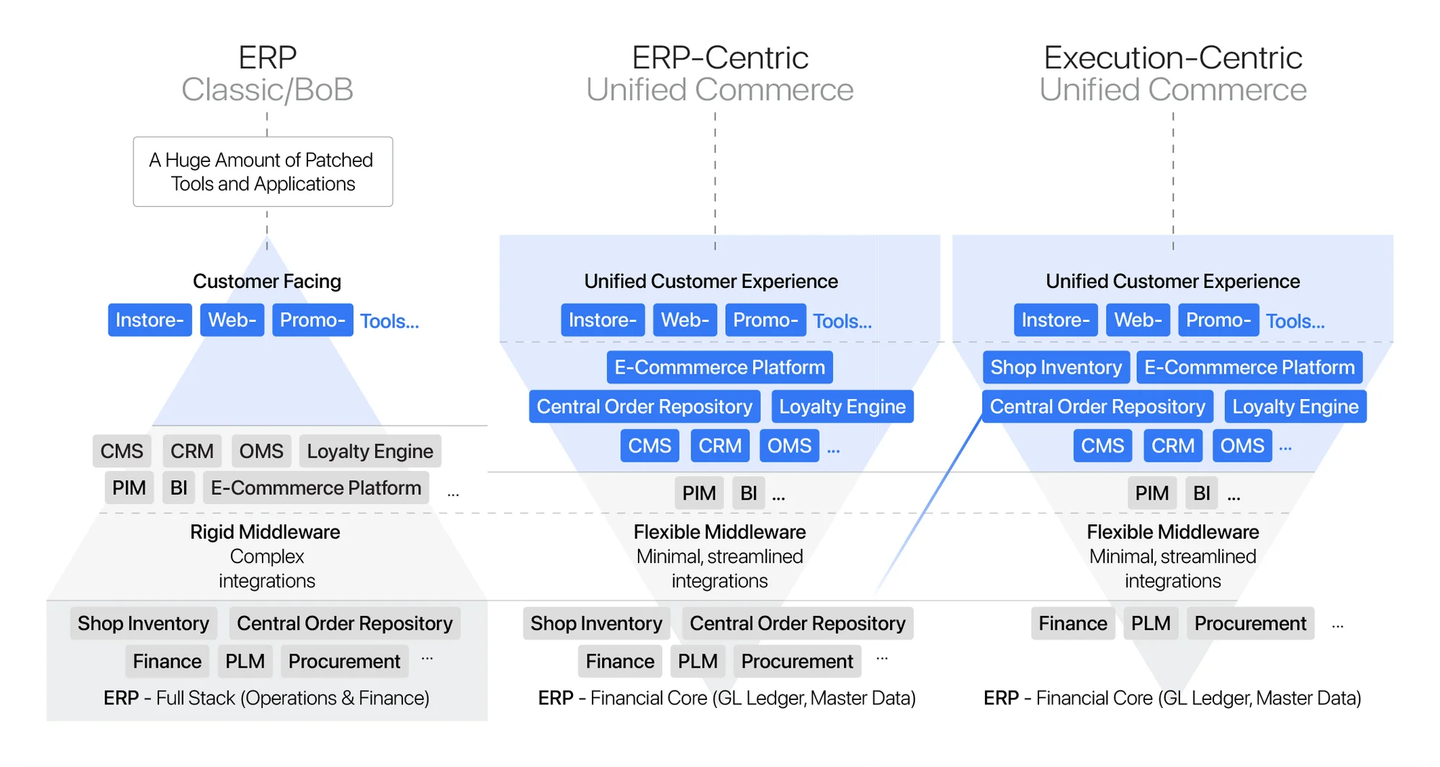

Visualizing the Shift: From Pyramid to Funnel

Adopting vision-driven leadership and Unified Commerce is a decisive step forward - but it’s not the final one. Even within this strategic shift, retailers face a critical architectural choice:

Retain ERP in a central operational role (ERP-Heavy) - or relegate it to a streamlined financial core (ERP-Light).

The visualization below illustrates how this choice shapes the entire retail technology stack - from ERP pyramids to unified customer-centric experience-driven funnels.

Historically, retailers built technology stacks as pyramids - with ERP at the base and multiple functional customer-facing tools layered on top.

In ERP-Heavy architectures, ERP continues to play an active operational role

Managing processes like order orchestration, inventory, and parts of customer logic. Note: this shared repository often results in overlapping data across platforms. Adding complexity in integration, maintenance, and data governance.

In contrast, ERP-Light architectures repositions ERP as a financial and administrative backend, focused on functions like finance, procurement, and master data. All real-time transaction and customer-facing logic shift to the Unified Commerce Suite, including the Central Order Repository.

Recommendations: Transitioning to Vision-Driven Leadership

For retailers to genuinely address and avoid the pitfalls of a FrankenStack, transitioning from traditional RFP checklist-driven decision-making to strategic, vision-based leadership is imperative. Key steps to facilitate this transition include:

Executive Alignment

Ensure technology decisions align with a clear, unified executive vision - rather than being fragmented by siloed decision-making.

Strategic Roadmapping

Replace detailed RFP checklists with strategic roadmaps that focus on business objectives—not just technical features.

Integration by Design

Choose architectures that are inherently unified - where customer, order, and channel logic live in one system, not scattered across disconnected tools.

Three Real-World Examples of How FrankenStacks Emerge

Despite good intentions, FrankenStacks often emerge unintentionally - the result of ERP-centric thinking, siloed decision-making, or excessive reliance on custom-built solutions. The following anonymized cases illustrate how these well-meant strategies can lead to fragmentation, inefficiencies, and rising operational complexity.

- 1.

Finance-Driven ERP Thinking Leads to Complexity

A multinational cosmetics brand expanding into a new market prioritized financial control and ERP compliance above speed and agility. What could have been a rapid and cost-effective rollout - budgeted at €50–€100K within a few weeks - turned into a 12-month implementation project costing over €1 million.

The reliance on ERP for end-to-end control introduced significant duplication of data, redundant processes, and a complex integration web. What began as a well-intentioned desire for control ultimately reinforced a rigid FrankenStack architecture that delayed operations and diluted customer focus.

Key Takeaways:

- ERP-centric thinking created unnecessary complexity and cost.

- Duplicated transactional data reduced data integrity and responsiveness.

- Prioritizing customer agility over ERP control could have avoided this outcome.

- 2.

Siloed Decisions Rebuild the FrankenStack, Piece by Piece

A European omnichannel retailer repeatedly selected new technology solutions based on attractive standalone presentations and department-level needs, with little strategic alignment across the broader architecture. Internally, the process was jokingly referred to as “PowerPoint heaven.”

Driven by tool-specific enthusiasm, the company gradually built a patchwork of Best-of-Breed platforms. Each component offered clear functionality, but together they lacked orchestration. The result was a disjointed customer experience - inconsistent across channels and hard to scale. Every new addition to the stack compounded complexity, delayed integrations, and increased technical debt.

Key Takeaways:

- Siloed tool selection led to fragmented architecture.

- Integration gaps degraded the customer journey and inflated operational cost.

- Architectural oversight and alignment are essential to prevent this pattern.

- 3.

Theoretical Perfection, Practical Dysfunction

A premium fashion retailer developed a highly customized system architecture using a mix of in-house tools and Best-of-Breed solutions. On paper, the design looked robust: feature-rich, adaptable, and fully tailored to the brand’s needs.

In reality, no tool fully delivered what was promised. Slight misalignments in data, workflows, and updates across components led to inconsistent behavior across the stack. While the design was technically impressive, it proved fragile in daily use - introducing failure points, slowing down innovation, and complicating maintenance

Key Takeaways:

- High customization without architectural coherence creates risk.

- ‘Almost-working’ tools undermine reliability and efficiency.

- Unified, customer-centric IT environments deliver more resilience and operational clarity.

A Pattern Too Familiar to Ignore

Each of these cases began with logical decisions, made in isolation. But taken together, they reveal a consistent pattern: short-term optimizations, driven by control or local needs, often result in long-term architectural debt. The more fragmented the stack becomes, the harder it gets to change - until strategic flexibility is no longer a choice, but a casualty. Recognizing this pattern is the first step; breaking it requires vision.

“Simplify the stack - Multiply the impact”

ERP-Centric vs. Unified Commerce: The Cost and Value Delta

ERP Update Cycles vs. Rapid Technological Evolution

ERP-centric architectures evolve slowly - relying on full replacements or major upgrades every 6–8 years. Unified Commerce, by contrast, develops continuously through seamless updates and integrations. This creates a growing delta in performance, agility, and cost-efficiency over time.

Why the Delta Grows: Structural Differences Behind the Curve

Although both architectures may support the same business goals, their underlying structure behaves very differently over time - especially when it comes to change, integration and operational stability.

Aspect | ERP-Centric Architecture | Unified Commerce-Centric Architecture |

|---|---|---|

Update Cycle | Major upgrades every 6-8 years. | Continuous layered updates (CI/CD) |

Integration Model | Custom integrations across multiple tools | Fewer tools, natively integrated within one platform |

Scalability | Limited by ERP structure and dependencies | Scales modularly across channels and touchpoints |

Adaptability to Change | Requires cross-system changes and testing | Built to absorb change across unified processes |

Operational Continuity | Modifications affect multiple layers and vendors | Seamless evolution with minimal business disruption |

Strategic Conclusions and Executive Considerations

Retail success today is no longer determined by channels, products, or promotions alone - but by the architectural decisions that enable or obstruct agility, integration, and customer-centricity. Many retailers operate within the limits of ERP-centric stacks without realizing that a fundamentally different structure is possible.

This insight has outlined how the FrankenStack - often a byproduct of control-based decisions and traditional system thinking - creates complexity, slows innovation, and inflates operational cost. Unified Commerce, and specifically ERP-Light architecture, offers a clear strategic alternative: one that aligns systems with how customer behavior and the world around us changes.

“For executive teams, the challenge now is not to recognize the problem - but to act on it.”

- 1.

Architecture is not neutral

Every system choice reflects - and reinforces - how your organization thinks, works, and serves customers.

- 2.

Suboptimization is a strategic risk

Fragmented technology may meet specific stakeholders’ needs, but undermines global performance, consistency, and adaptability.

- 3.

Vision must lead procurement

If your strategy starts with a checklist, you’ll end with a compromise. True customer-centricity requires alignment at the architectural level.

- 4.

The cost of inaction compounds over time

FrankenStacks don’t collapse overnight - but they erode speed, clarity, and strategic optionality until it’s too late.

Final thought: Unified Commerce isn’t a toolset - it’s a structural commitment to serving the customer, not the system.

References

- McKinsey - Retail Transformation Study, 2024

- GartnerIT - Complexity Benchmark, 2024

- Deloitte - Retail IT Survey, 2024

- IDC - Retail Insights, 2024

- Forrester - Predictions 2025: Retail

Don't miss these

Designing Retail IT Architecture for Agility

Enable enterprise growth with a retail IT architecture built for agility, scalability, and faster decision-making across retail.

Strategic Cost Assessment

Compare iOS and Android in enterprise retail through the lens of total cost of ownership, security, compliance, and operational performance.

From Touchpoints to Increased Transactions

Turn every customer touchpoint into measurable business impact with a unified commerce approach that drives conversion, growth, and long-term value.